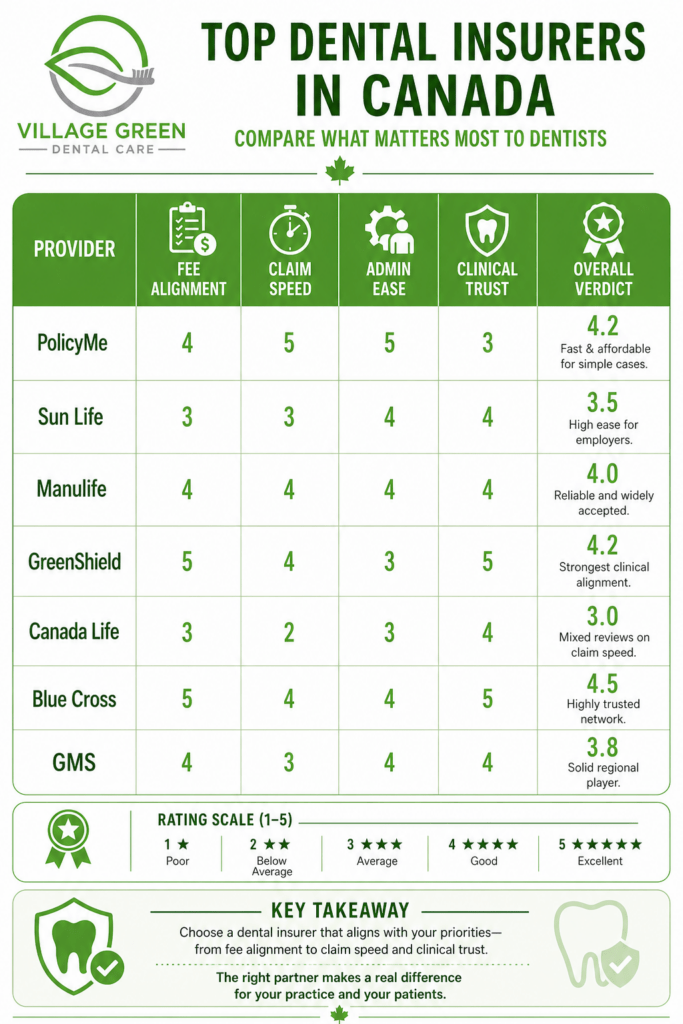

Dental insurance in Canada is considered a necessity, but any practicing dentist will give you a more complex response. Corporate providers such as Sun Life Financial, Manulife, Green Shield Canada, Canada Life, Blue Cross, and Group Medical Services (GMS) dominate the market but the real question is: does dental insurance really work to the benefit of the patients or simply to their assistance?

The Key Evaluation Factors Dentists Care About

1. Fee Guide Alignment (2026 Provincial Fee Guide)

One of the most critical factors in Dental insurance reviews in Canada is whether insurers align with the latest provincial dental fee guides. Dentists say that, although many providers have stated that they are aligned, not all move to the present 2026 fee structures. Partially aligned can cause patients to face surprising out-of-pocket expenses, particularly when undergoing big treatments.

2. Adjudication Ease ( Speed of Approving Claim )

Clinically, a smooth processing of claims is necessary. Dentists can use providers whose adjudication systems are real-time and so submit claims electronically and get approvals instantly. Nonetheless, the slower insurers are still subjected to manual processing, which slows down the reimbursement and annoys both patients and clinics. This directly impacts dental insurance approval satisfaction.

3. Pre-Determination for Major Procedures

Pre-determination is important with such treatments as crowns, bridges, or root canals. Dentists point out that there are those insurers who can give approvals in a few days and others take weeks. This delay tends to make patients put off the care they require- creating issues of deteriorating oral health.

4. Medical Necessity Challenges

Another growing concern is how frequently insurers question clinical recommendations. According to dentists, some providers are becoming more stringent regarding what is considered as medically necessary. This may result in refusal of procedures that the dentists may deem necessary, putting patients in a challenging financial and health predicament.

5. Transparency & Patient Portals

The current dental insurance must provide real time and transparent coverage balances. Though the majority of significant insurers have digital portals, their usability is quite diverse. Absence of transparency tends to create confusion with regard to benefits that are left, co-payments and yearly limits.

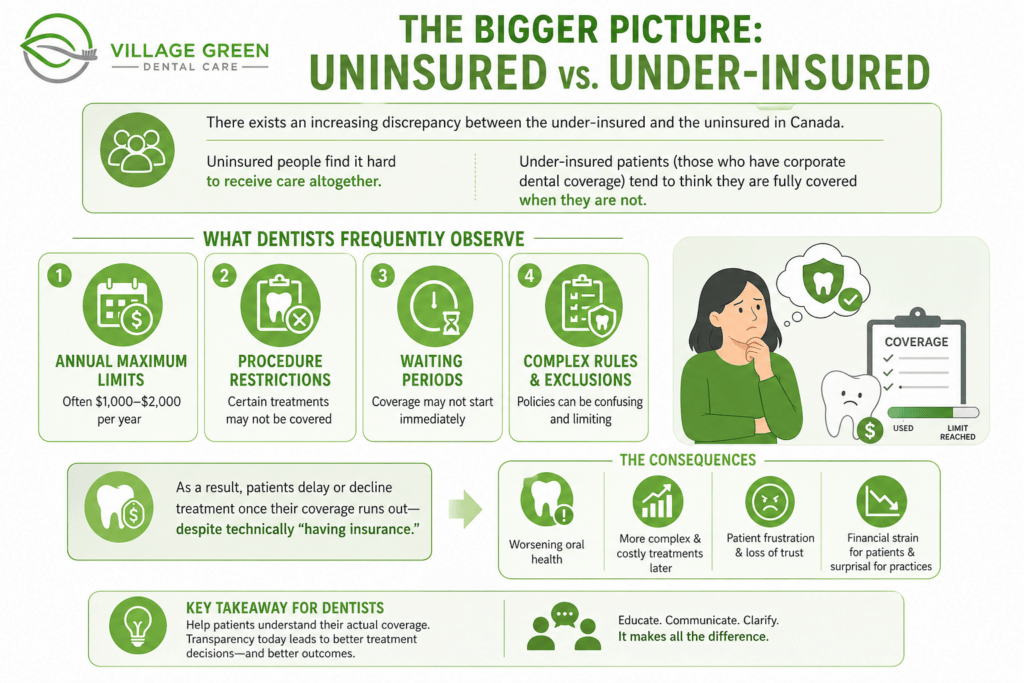

The Bigger Picture: Uninsured vs. Under-Insured

It is at this point that the discussion is more interesting- and useful to journalists.

There exists an increasing discrepancy between the under-insured and the uninsured in Canada. Whereas uninsured people find it hard to receive care altogether, under-insured patients (those who have corporate dental coverage) tend to think that they are fully covered when not.

Dentists frequently observe that insurance plans come with:

- Annual maximum limits (often $1,000–$2,000)

- Procedure restrictions

- Waiting periods

As a result, patients delay or decline treatment once their coverage runs out—despite technically “having insurance.”

What Dentists Actually Recommend

However, the majority of dentists do not consider dental insurance an all-encompassing safety net as many people think. They instead promote a mixed method of approach:

1. Have Dental Insurance to attend to Routine Care

Preventive care, such as cleanings, exams, and minor procedures, is good with insurance.

2. Build a “Dental Emergency Fund”

Dentists highly suggest the personal savings be put aside in case of unanticipated or significant treatments. This lessens the dependence on insurance endorsements and provides care in a good time.

The Real Question- Is Dental Insurance Worth It?

Yes–but realistically. Canadian dental insurance is beneficial especially in preventive services. But it is not good enough as an all-purpose dental solution. The variability in dental fee guide alignment, claim approvals, and transparency means patient experiences differ significantly across providers.

For journalists exploring Dental insurance reviews in Canada, the real story isn’t just about which company performs best—it’s about understanding the gap between coverage and actual care.

Final Takeaway

Dental insurance is helpful, but not sufficient. As dentists emphasize, the smartest approach for Canadians is to combine insurance coverage with personal financial preparedness.

Because when it comes to oral health, waiting for approval isn’t always an option.

{kind=link}